-

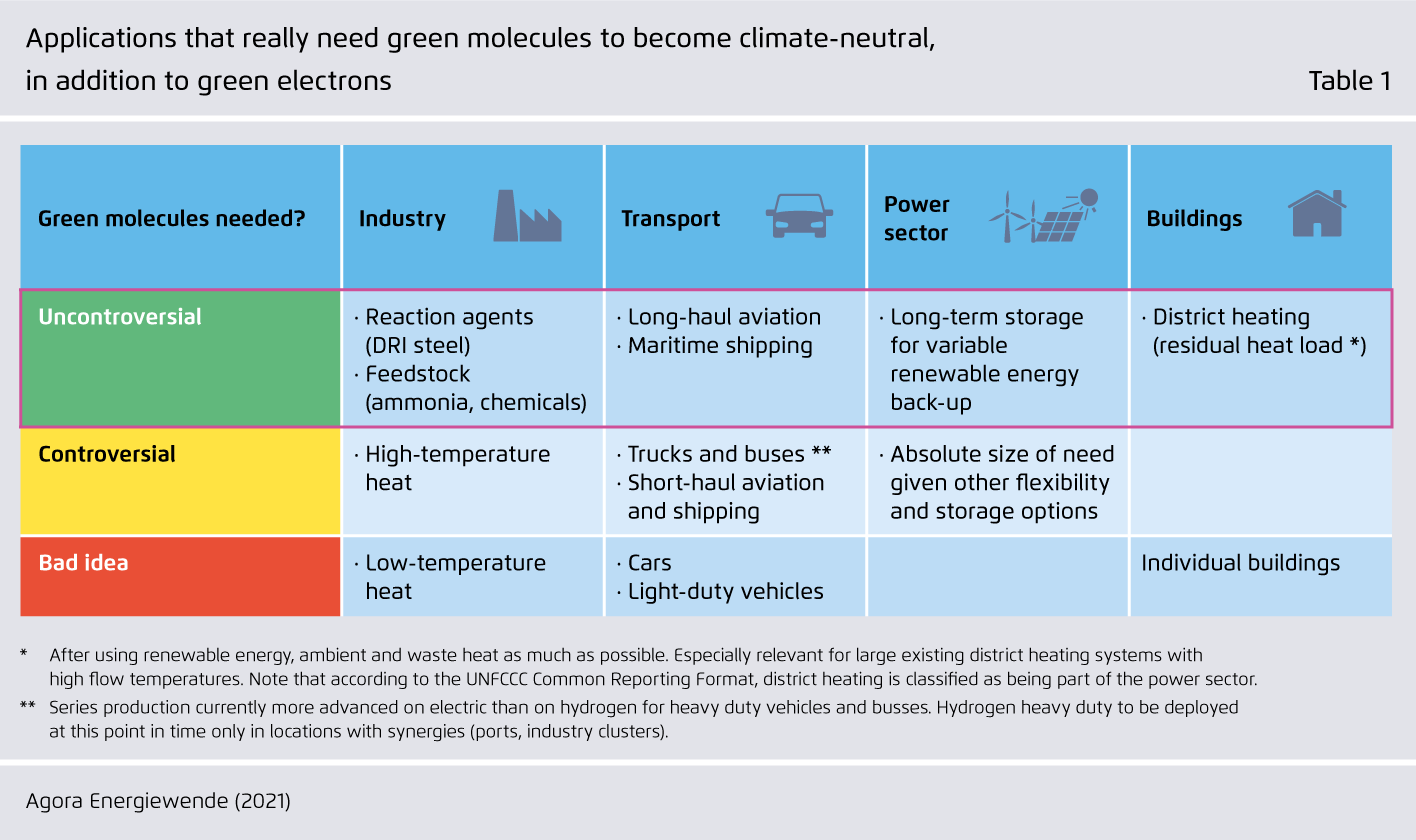

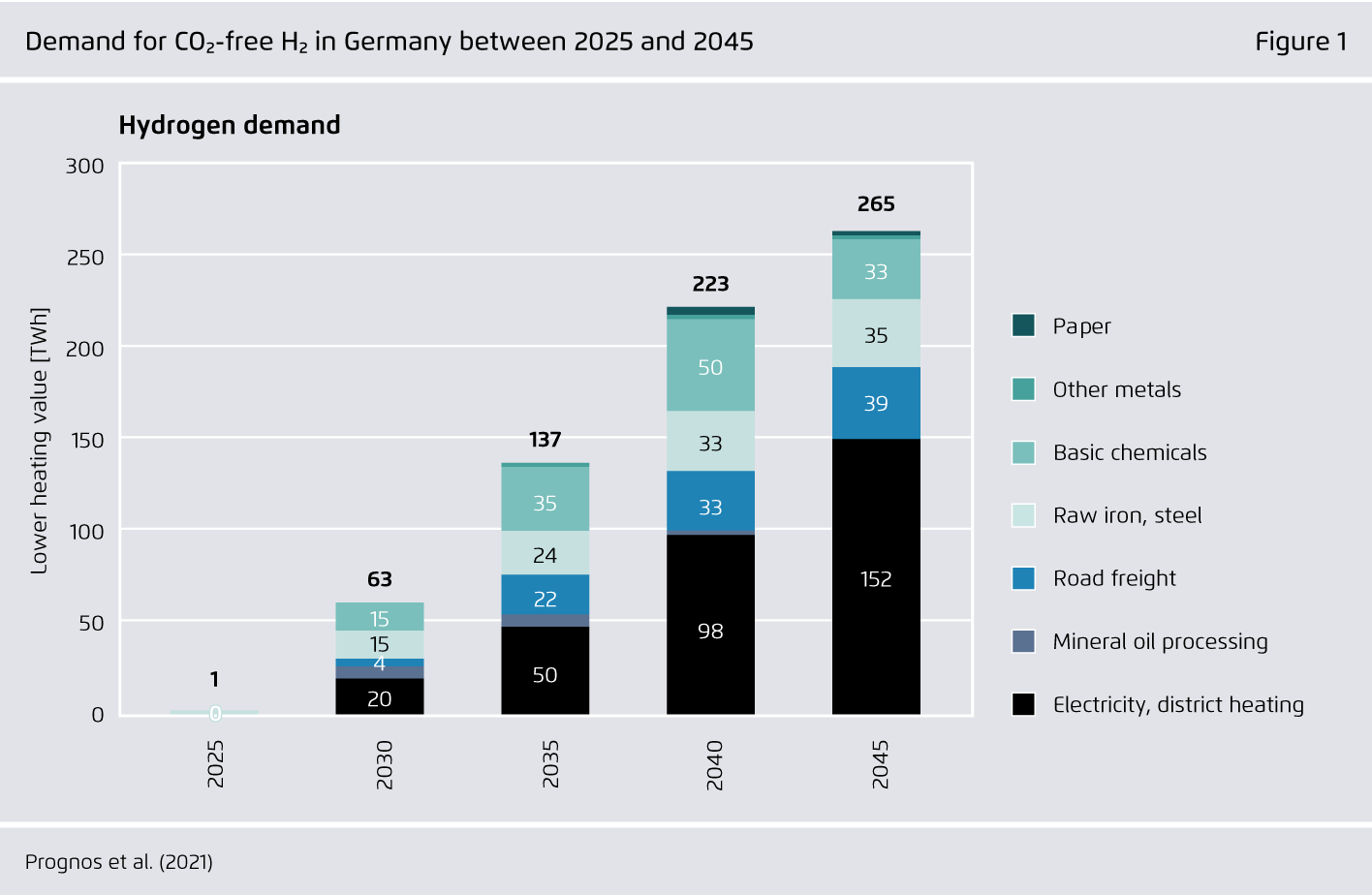

There is a limited set of applications in all sectors that urgently need renewable hydrogen to become climateneutral.

These applications include steel, ammonia and basic chemicals production in the industrial sector, as well as long-haul aviation and maritime shipping. The power sector needs long-term storage to accommodate variable renewables, and existing district heating systems may require hydrogen to meet residual heat load. Accordingly, renewable hydrogen needs to be channelled into these no-regret applications.

-

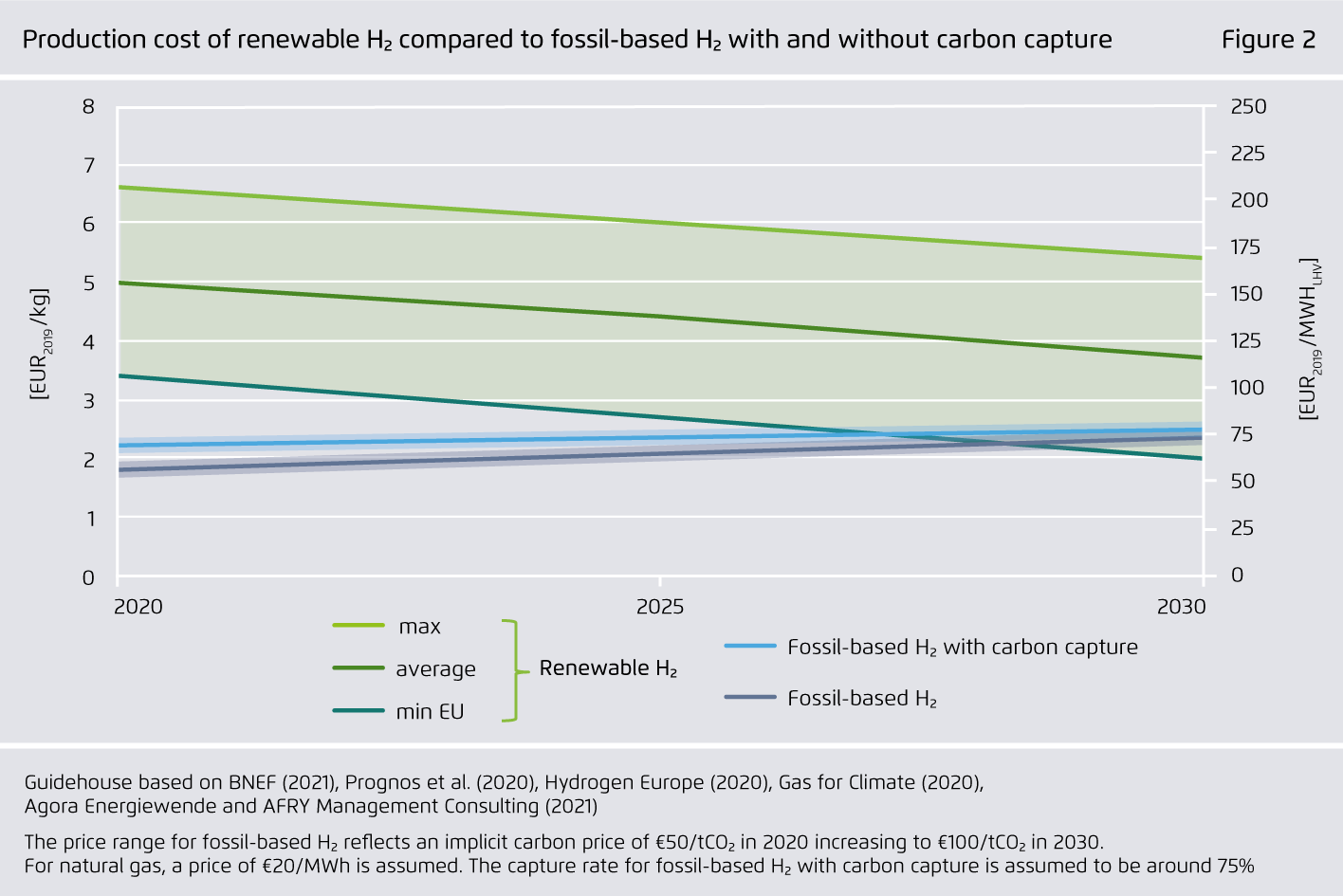

Ramping up renewable hydrogen will require extra policy support that is focused on rapid cost reductions.

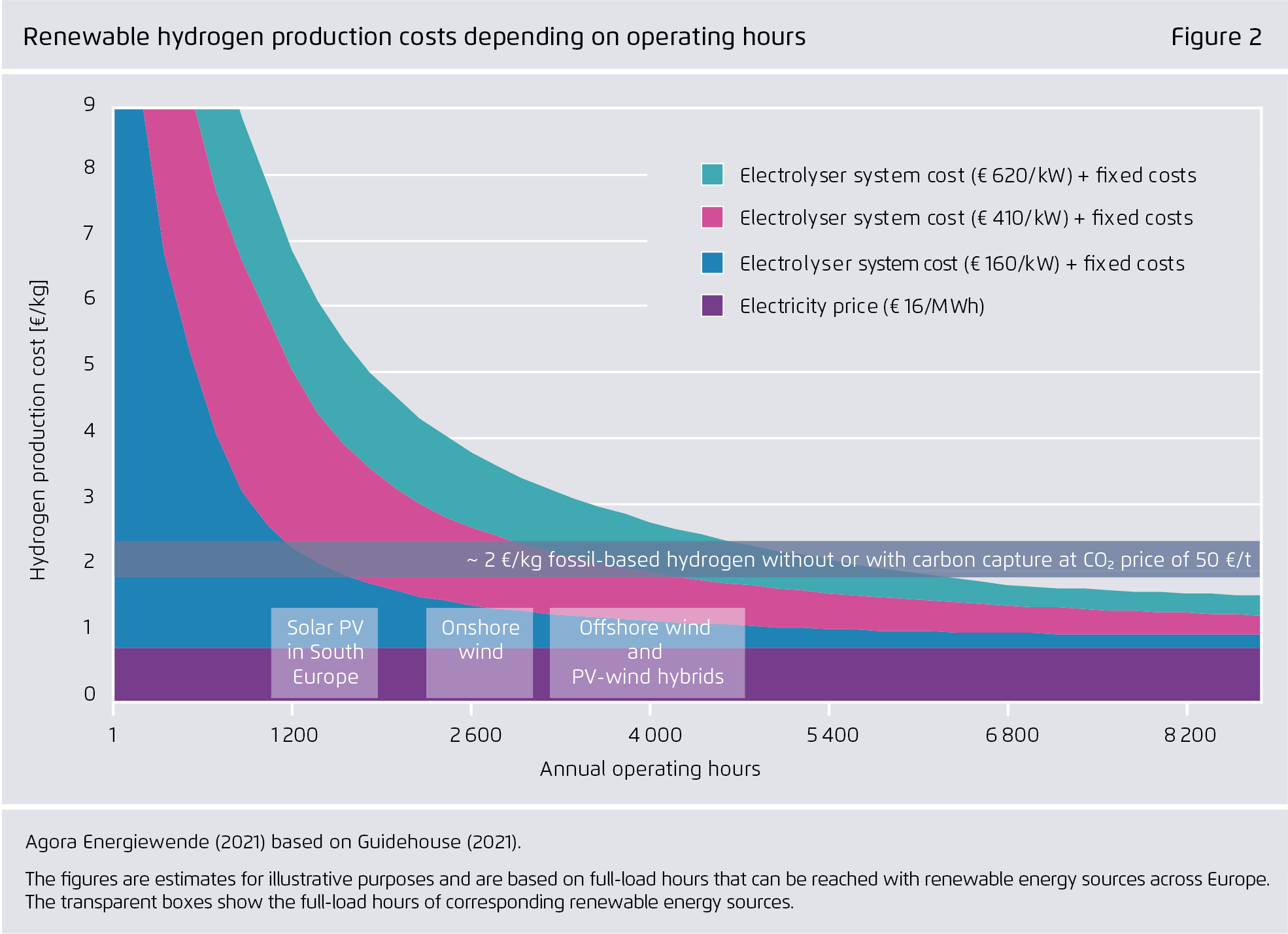

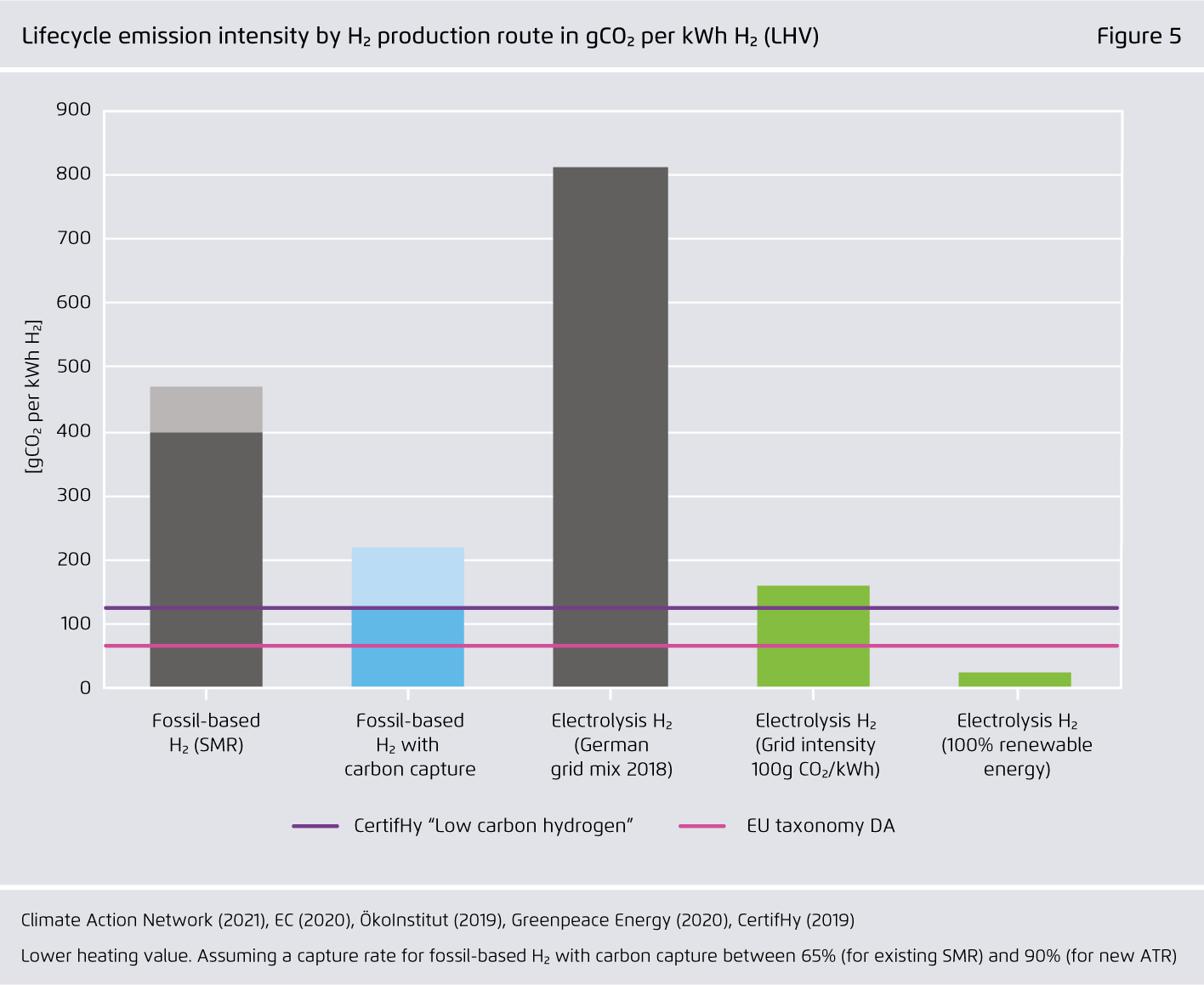

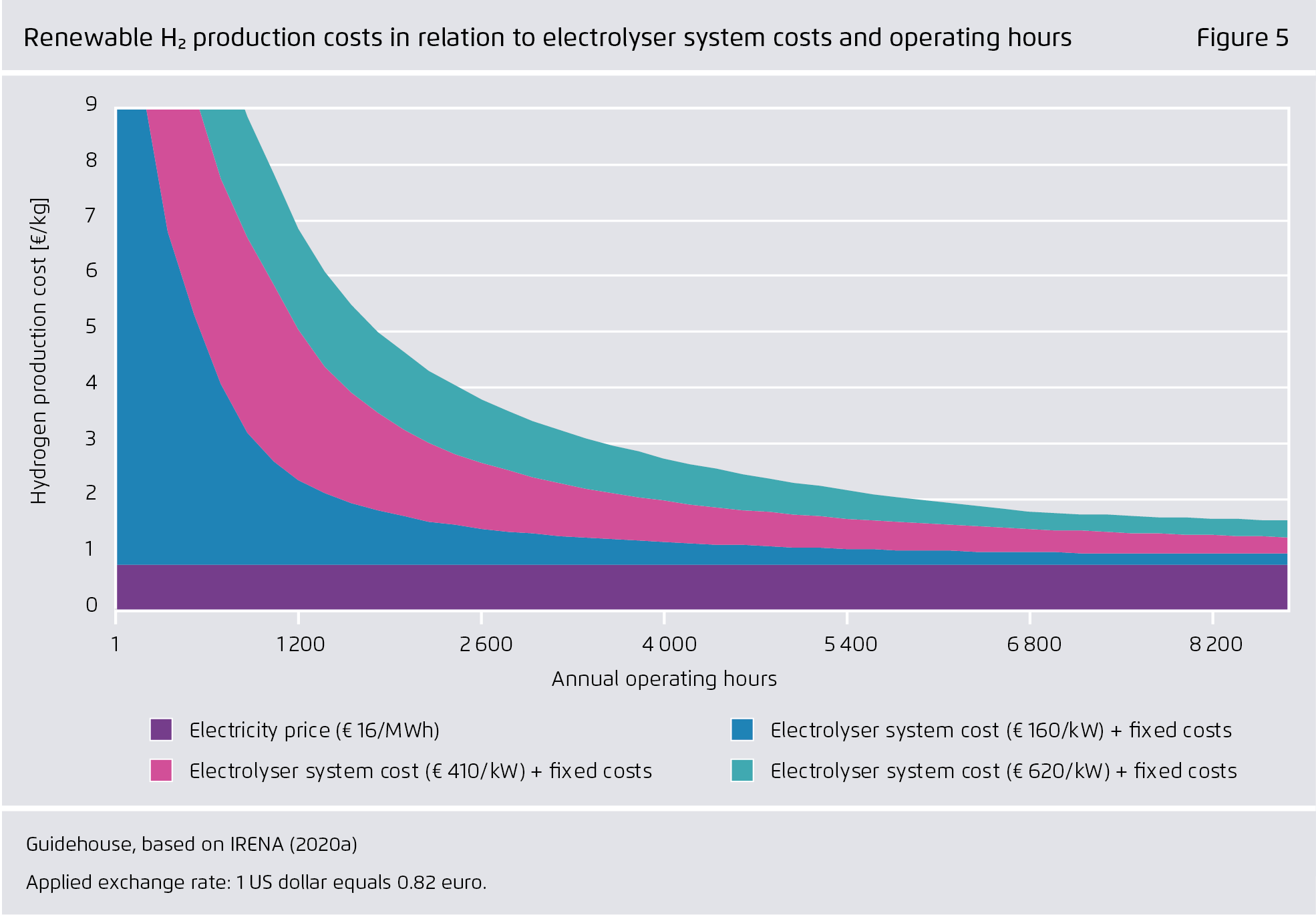

While renewable electricity (the main cost component of renewable hydrogen) is already on track to become cheaper, electrolyser system costs also need to be reduced. Cheaper electrolysers will come through economies of scale and learning-by-doing effects; however, predictable and stable hydrogen demand is prerequisite for electrolyser manufacturers to expand production and improve the technology.

-

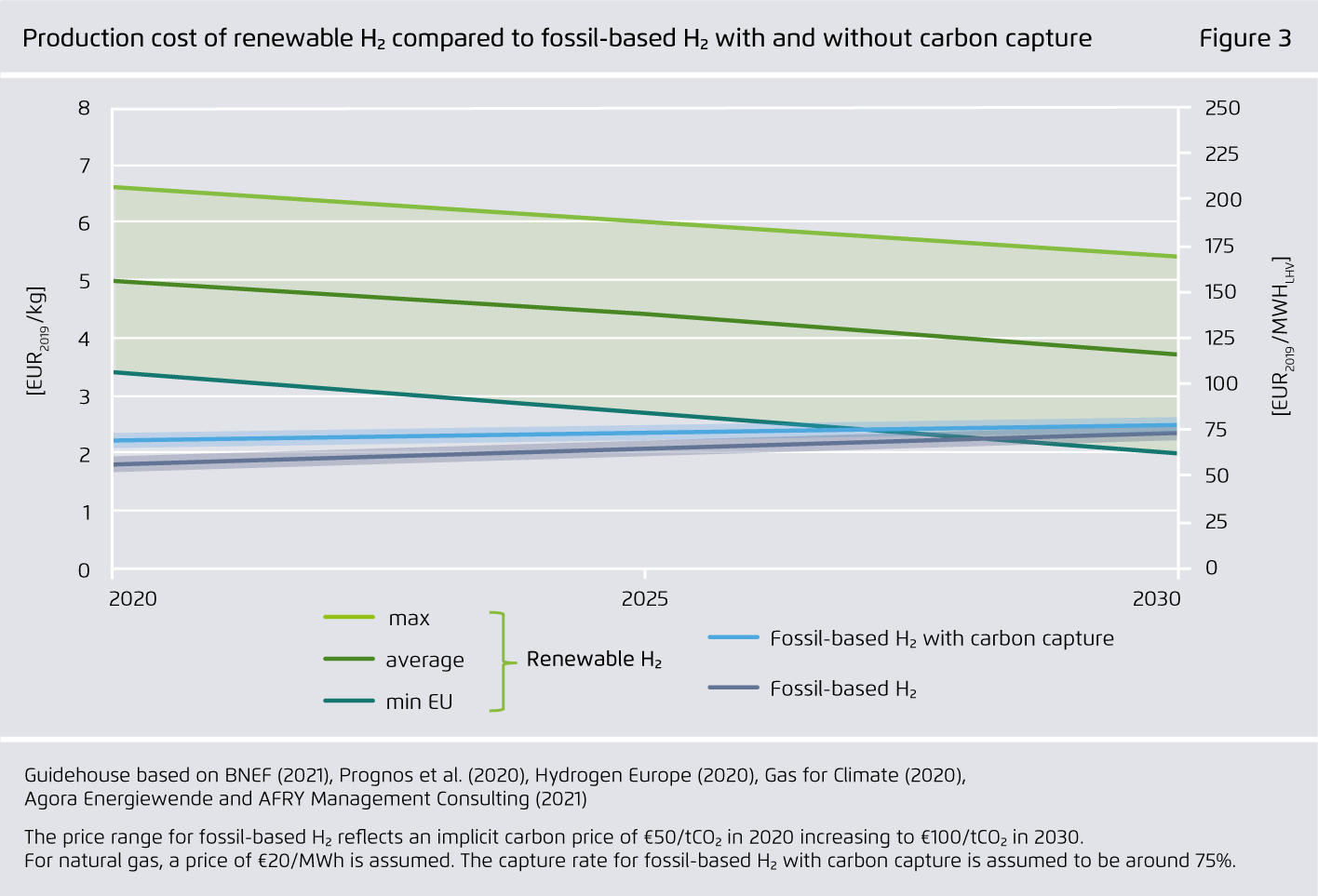

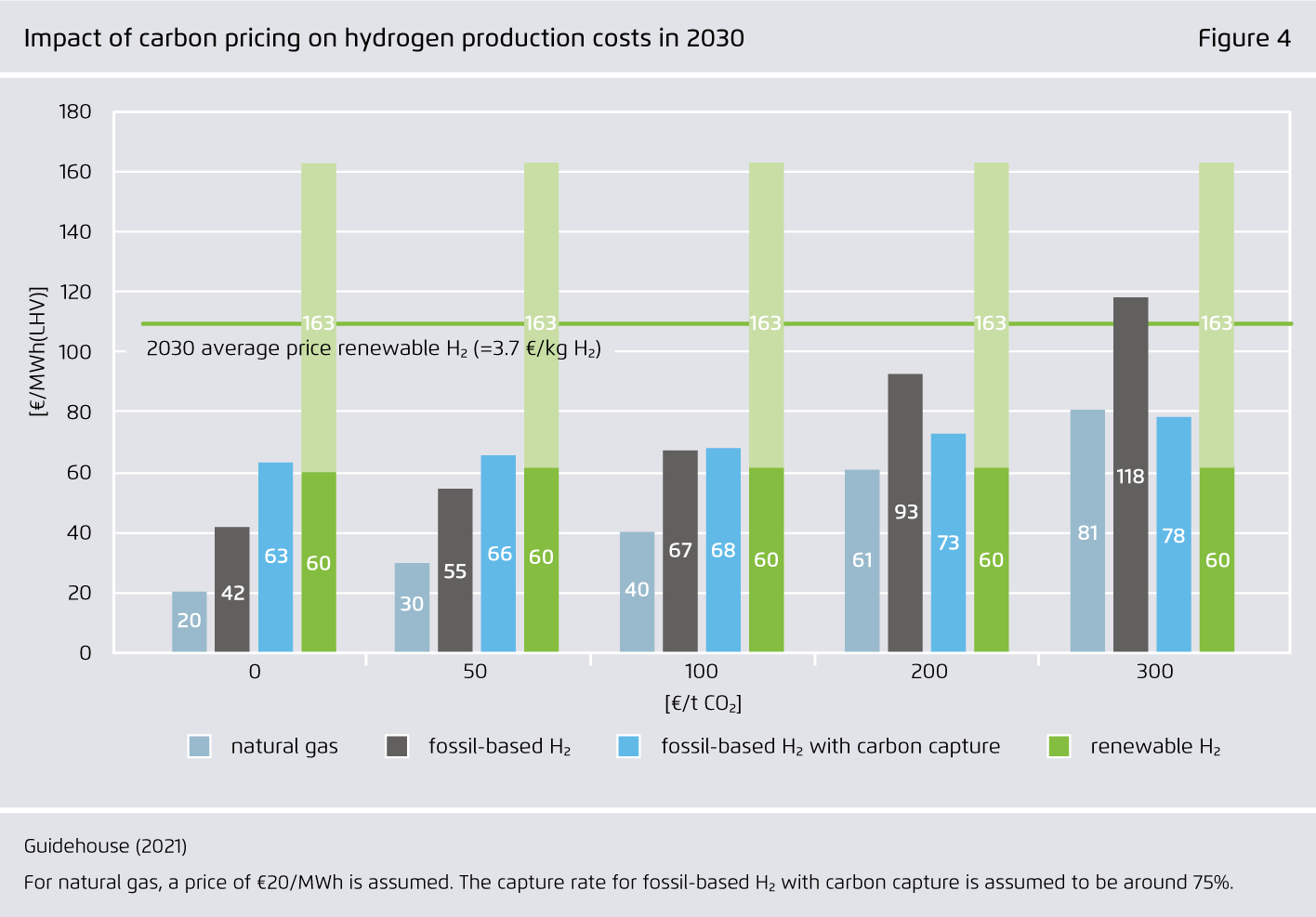

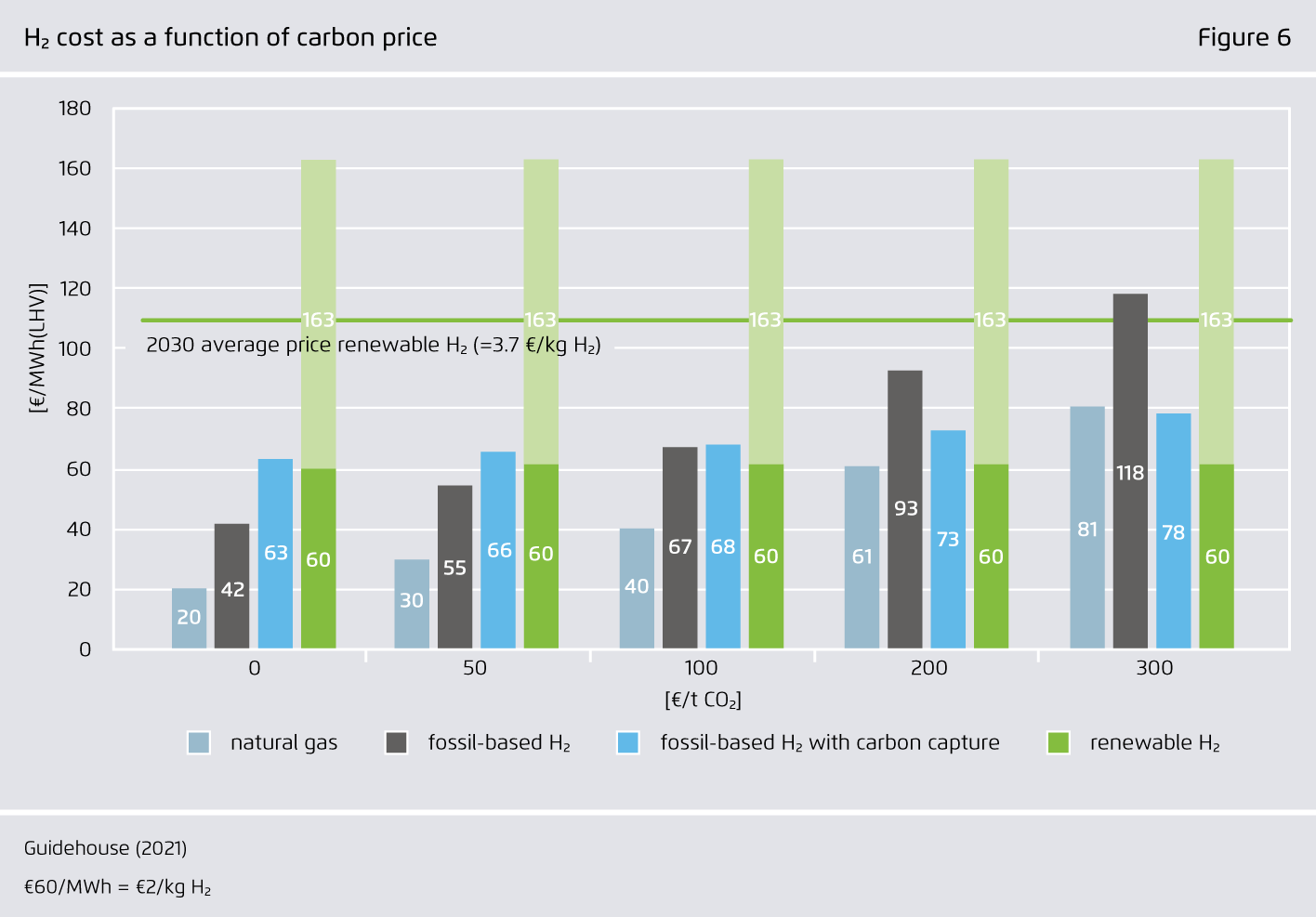

CO₂ prices in the 2020s will not be high enough to deliver stable demand for renewable hydrogen, underscoring the need for a hydrogen policy framework.

Even at CO₂ prices of €100 to 200/tonne, the EU ETS will not sufficiently incentivise renewable hydrogen production, making additional policy support necessary for a considerable period of time. Among potential policy options, a general usage quota for renewable hydrogen would not be sufficiently targeted to induce adoption in the most important applications.

-

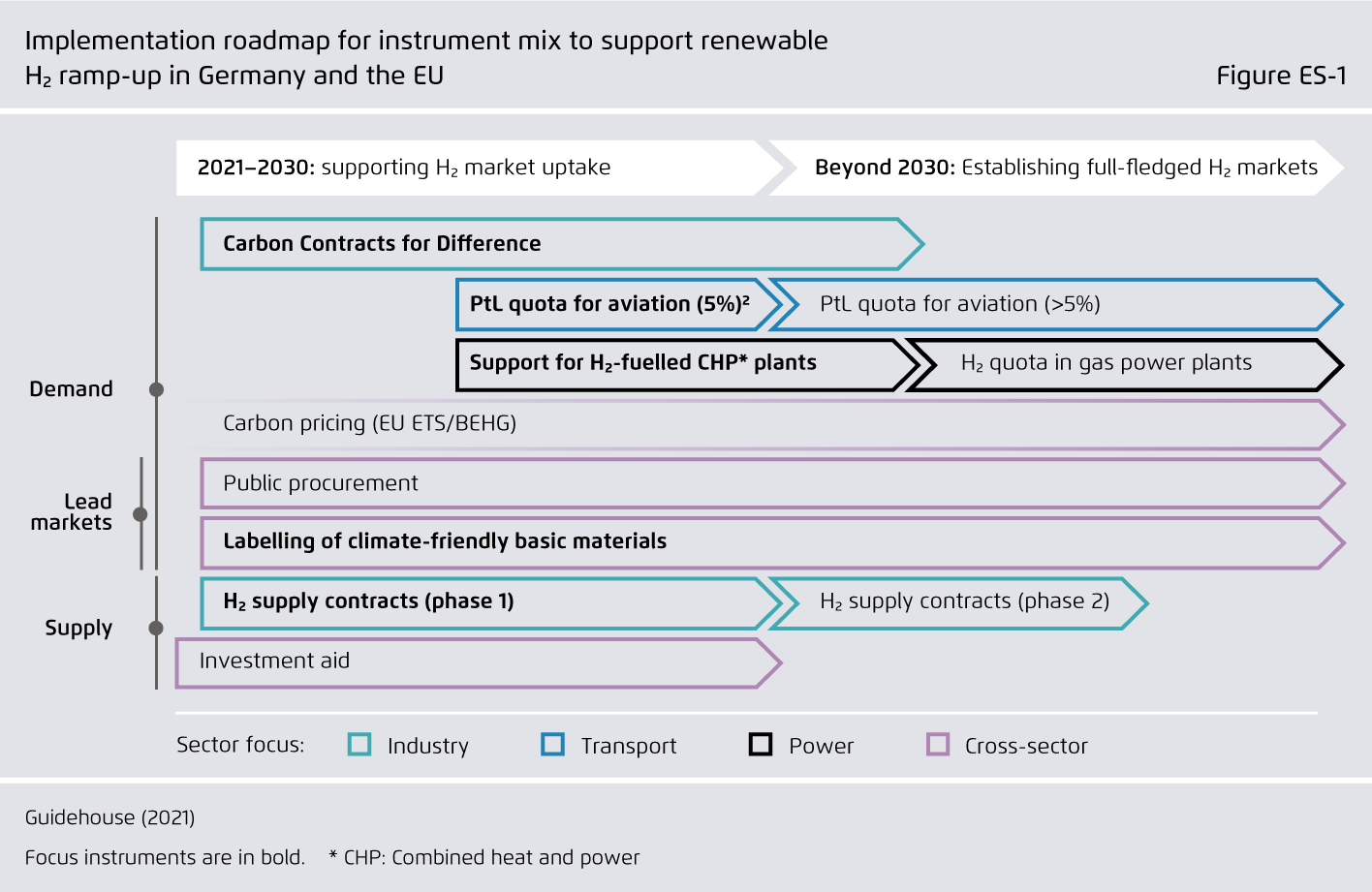

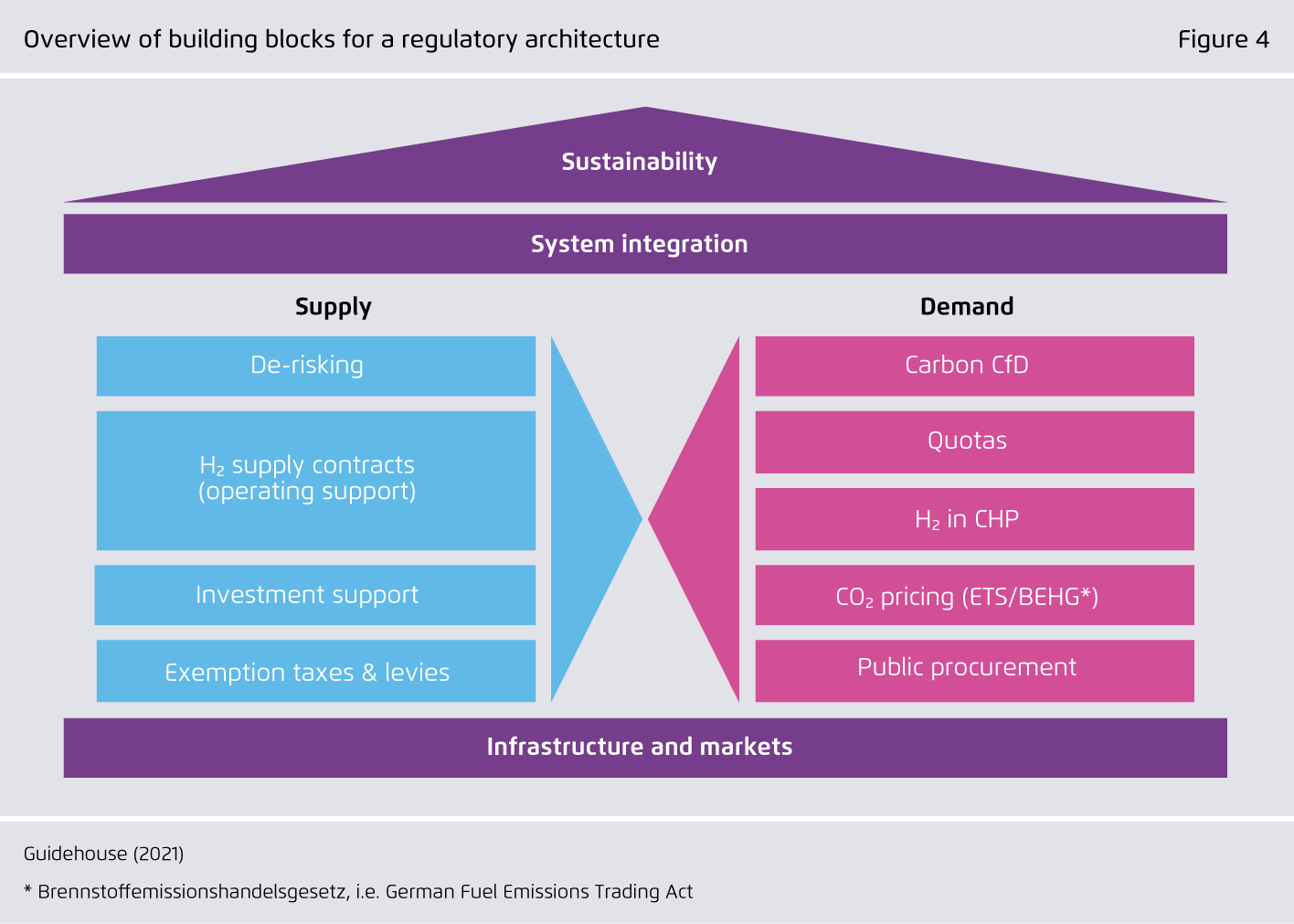

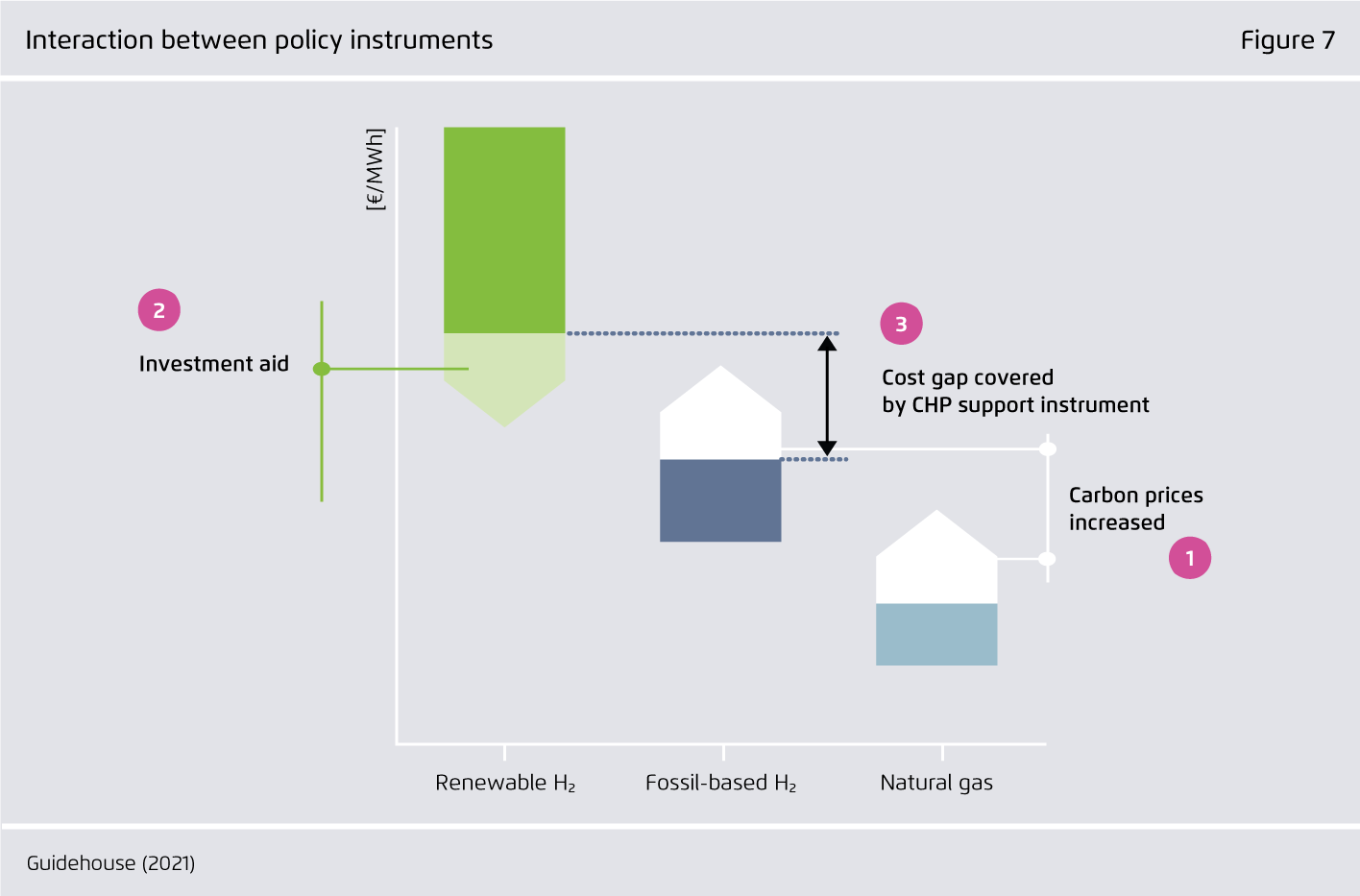

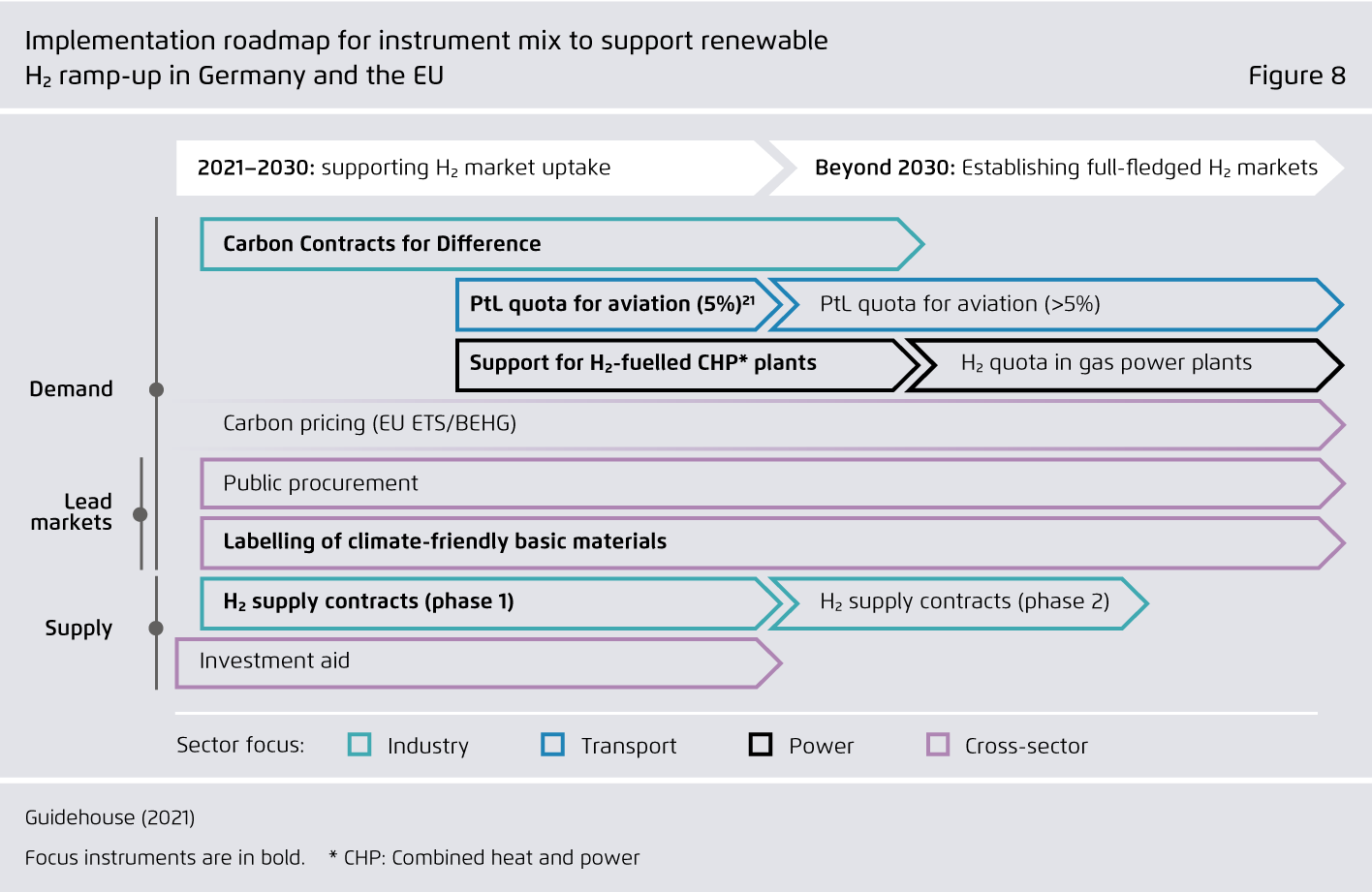

A policy framework to ramp up the market for renewable hydrogen should initially target the applications where hydrogen is clearly needed and a no-regret option.

Several policy instruments should be deployed in concert to achieve this aim – namely, carbon contracts for difference in industry; a quota for aviation; auctions to support combined heat and power plants; measures to encourage markets for decarbonised materials; and hydrogen supply contracts. These instruments will also need to be complemented by regulations that ensure sustainability, appropriate infrastructure investment, system integration, and rapid renewables growth.

Making renewable hydrogen cost-competitive (Study)

Policy instruments for supporting green H₂

")

Preface

Hydrogen will be a key enabler of climate neutrality in various sectors. In line with this insight, policy makers in Europe have been actively adopting hydrogen development strategies.

Unfortunately, as clearly acknowledged in the European Commission’s 2020 Hydrogen Strategy, renewable hydrogen production is economically uncompetitive today – even with record carbon certificate prices – and is expected to remain uncompetitive until the 2030s. To put it succinctly: there is currently no natural market demand for fully decarbonized hydrogen, nor is such demand anticipated to materialise prior to the end of this decade.

European industrial policy is required to fill this gap – and, in our view, action should be taken quickly (i.e. as part of the Fit-for-55 Package, and the revision of state aid guidelines).

To better understand hydrogen’s policy support needs and their effects, Agora Energiewende and Guidehouse have examined the policy instruments most promising for bridging the cost gap between renewable hydrogen and its fossil counterparts. Based on our findings, in this study we present a policy instrument mix and roadmap designed to catalyse the renewable hydrogen ramp-up.

Key findings

Bibliographical data

Downloads

-

pdf 4 MB

Making renewable hydrogen cost-competitive

Policy instruments for supporting green H₂

All figures in this publication

Applications that really need green molecules to become climate-neutral, in addition to green electrons

Figure Table 1 from Making renewable hydrogen cost-competitive (Study) on page 10

Share:

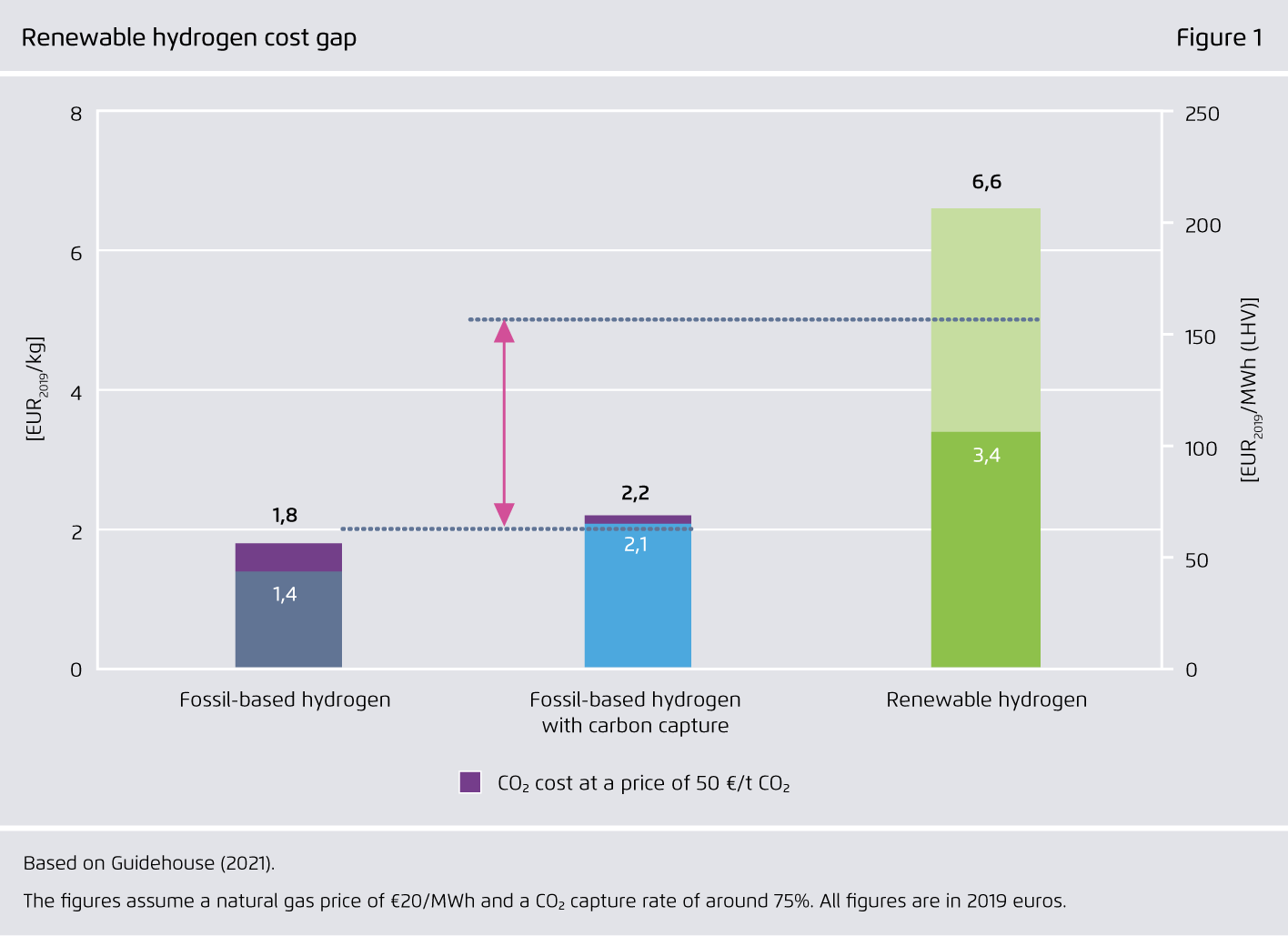

Renewable hydrogen cost gap

Figure 1 from Making renewable hydrogen cost-competitive (Study) on page 11

Share:

")