- While recent global additions of wind and solar are encouraging, progress of renewable energy development in South, Southeast and East Asia has been insufficient. The share of solar and wind power in most countries in this region is below six percent today, despite the falling cost of clean energy technologies. Accelerating the deployment of wind and solar power within the next five years is crucial to meeting the region’s climate mitigation goals.

- To be aligned with a 1.5°C-compatible pathway, renewables in the region will need to supply 50% of total electricity by 2030, with 30% coming from wind and solar. This corresponds to annual capacity additions of at least 55 GW for solar and 20 GW for wind, compared to just 11.9 GW solar and 1.5 GW wind installed in 2021.

- Accelerating the integration of wind and solar power in the region requires a paradigm shift towards increased system flexibility and removal of policy, regulatory, and market barriers. Some solutions include de-risking mechanisms and accelerated permitting processes which can kick-start wind and solar deployment while supportive grid codes can aid in their system integration.

Sun and wind for net zero - benchmarking renewables growth in South, Southeast and East Asia

- Key findings

- Curbing emissions means turning pledges into action

- The next five years are crucial to achieve climate targets

- Wind and solar additions in large parts of Asia have been insufficient

- Wind and solar will need to supply 30% of total electricity by 2030

- The region should add 75 GW of wind and solar every year

- Policy, regulatory and market reforms can accelerate wind and solar growth

Key findings

The message arising from global net-zero scenarios is clear: getting to climate neutrality requires adding 1000 GW of wind and solar power every year until mid-century, while also gradually electrifying most end-use sectors (IEA, 2022; IRENA, 2022). While useful, such global top-down assessments are often unable to capture local specifics, and thus provide little help to those seeking to develop energy transition roadmaps consistent with their domestic climate targets. What do these global numbers concretely mean for policy makers in South, Southeast and East Asia?

To answer this question, Agora Energiewende reviewed more than 35 long-term energy scenarios from Japan, South Korea, Vietnam, Indonesia, the Philippines, Thailand, Pakistan, Bangladesh, and Taiwan, China*. These scenarios are bottom-up analyses carried out by local institutions in close consultation with various stakeholders. They consider specific local constraints and political economy developments, including technology costs, resource potentials and social development targets. As such, they complement global analyses such as those by the IEA and IRENA.

These economies combined cover about 14% of the world’s population (1.1 billion people), 10% of global electricity demand, and 10% of global power sector emissions. Although the region’s developing and emerging economies emit today less greenhouse gas emissions per capita than the world average, these emissions could double in the next decades without concerted decarbonisation efforts.

This interactive publication offers an overview of the transition to a renewables-based, flexible power system, benchmarks wind and solar growth against the region's climate pledges – and provides recommendations to accelerate the transition.

Curbing emissions means turning pledges into action

The economies of South, Southeast, and East Asia are diverse, with huge variations in natural resources, levels of development, and energy market structures. Yet, they share some key challenges: climate change impacts jeopardising development goals, and a prevalent reliance on fossil fuels combined with relatively low rates of renewable energy deployment.

South and Southeast Asia are home to some of the fastest growing economies in the world – with increasing energy demand to match, potentially growing by as much as 80% by 2050. On the other hand, the more mature economies of East Asia are already home to some of the highest per capita greenhouse gas emissions globally.

Despite encouraging recent progress with many Asian governments setting net-zero targets and some adopting coal phase-down targets, the region overall lacks credible policy implementation plans. Persistent investments into fossil fuels and relatively low rates of renewable energy deployment are common traits across the region.

The next five years are crucial to achieve climate targets

Limiting global warming to 1.5°C requires immediate action to avoid overshooting temperature limits that could lead to irreversible changes to our natural environment and an increased burden on the region to adapt to climate impacts. The International Panel on Climate Change (IPCC) highlights that halving emissions by 2030 is imperative, and that the policy and technology options to do so are already available. For the energy sector, this will mean using energy and materials more efficiently, reducing fossil fuel use, and widespread electrification.

At the vanguard of this transition are wind and solar power. Their declining costs, coupled with advancements in efficiency measures and flexibility technologies such as energy storage, mean that wind and solar power are already competitive and represent sustainable alternatives to fossil fuels. For example, utility-scale solar is already the cheapest source of electricity generation in several economies in the region, for example in Vietnam.

A swift decarbonisation of the electricity system is essential for the decarbonisation of the transport, buildings, and industry sectors. Indeed, electricity is poised to displace fossil fuels in all sectors, either directly, e.g. in electric vehicles and power-to-heat applications, or indirectly through the use of fuels generated by renewable electricity, such as renewable hydrogen. Reciprocally, these sectors, once electrified, can provide additional flexibility, such as smart charging, to facilitate the system integration of variable renewables.

Wind and solar additions in large parts of Asia have been insufficient

Wind and solar will need to supply 30% of total electricity by 2030

The region should add 75 GW of wind and solar every year

Translating renewable power shares into installed wind and solar capacities (GW) depends on several country-specific factors: resource availability, other competing low-carbon technologies (in particular hydropower), power demand growth, current state of the market, and other factors.

Solar deployment should increase fivefold in the region by 2030 to reach climate targets.

For wind, the analysed...

The installed wind power capacity should grow tenfold compared to 2021.

Policy, regulatory and market reforms can accelerate wind and solar growth

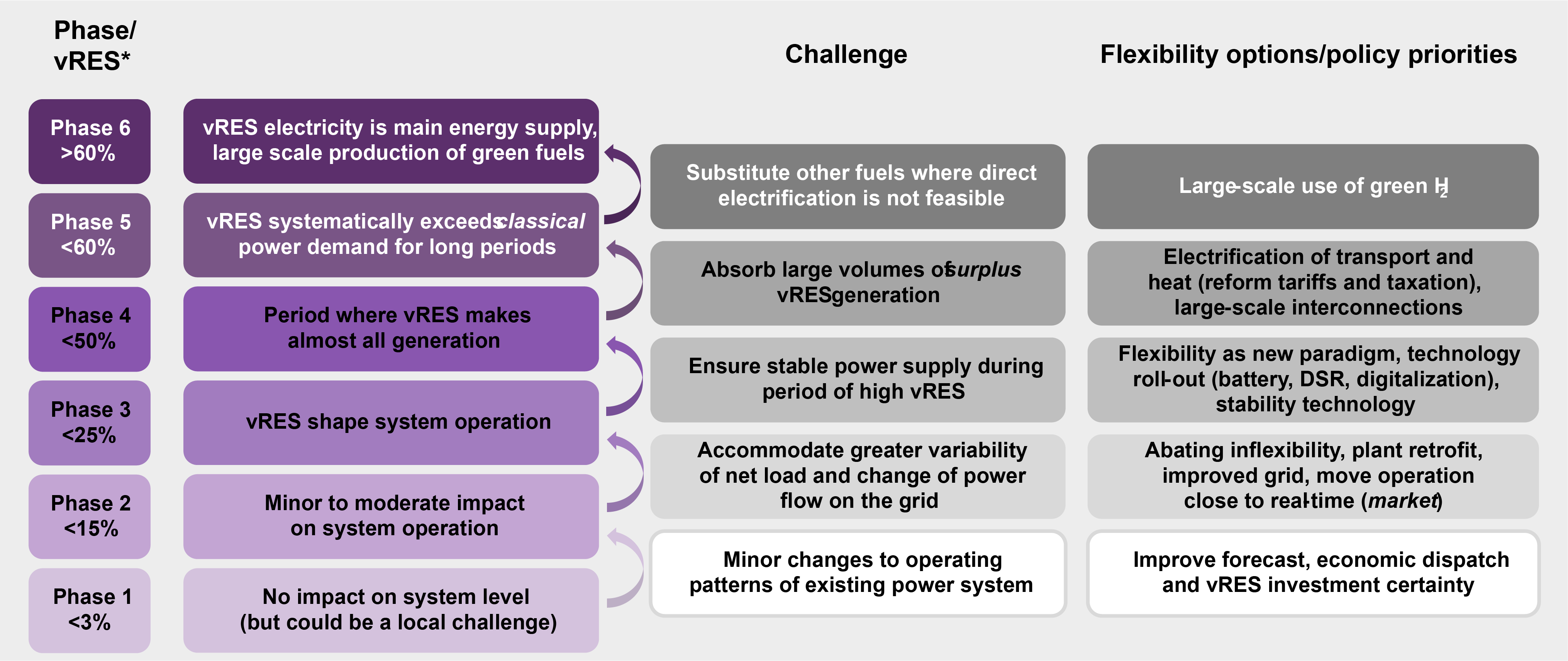

The growth of wind and solar power will depend on whether future regulatory and political economy choices are successful in creating an attractive investment environment to significantly scale-up wind and solar deployment. Discussions around wind and solar integration into power systems are often still marred by misconceptions. Prioritising policy that succeeds in accelerating the deployment and integration of variable renewable power must therefore be tackled gradually, depending on its share in the system.

Source: Adapted from IEA (2017) *Share of vRES generation. Numbers are indicative and depend on the specifics of the power system

In countries where the share of renewables is low (“Phase 1” countries with a share of variable renewables below 5%), attracting investments into wind and solar through supportive de-risking mechanisms, and designing supportive grid codes for the integration of renewables should be priorities. Permitting processes that delay projects need to be streamlined. That could include consolidating approvals under a single authority, improving investor and stakeholder confidence and minimising investor risks. Allowing priority dispatch for renewables would offer a clear signal that market preference is given to clean sources of electricity, and can be very effective if combined with a structured retirement plan for fossil assets.

In countries where renewables uptake has already progressed (“Phase 2” countries with a share of variable renewables below 15%), system operations start to be impacted. The focus should be on managing integration challenges through a combination of regulatory and market refinements that minimise system inflexibilities. The question of land availability also starts to be especially prevalent in densely populated countries such as in Bangladesh (1,330 people per square meter), Japan (340 per square meter) and Korea (515 per square meter). Exploring alternative areas, for example solar PV on agricultural land, or floating PV on freshwater reservoirs can help widen the options for renewables developers.

Typically, significant integration challenges begin to occur at wind and solar shares greater than 15% (“Phase 3”). Power system operations and planning will need to be fundamentally transformed to adapt to the variability of renewables and move towards a “flexibility paradigm”. The concept of ‘baseload’ generators begins to become obsolete.

In the longer run, a more systematic approach to renewable integration will be required that fosters flexibility investments such as grid development, storage and renewables-based electrification of end-use sectors (sector planning). This approach requires much more integrated planning processes, both multi-sectorial and long-term. However, in most scenarios, the large roll-out of battery storage technologies and electrification of end-use sectors become relevant only after 2030.

The measures needed to accelerate the renewable energy transition vary between countries, and depend on the state of the transition.

Footnotes

* This publication including its data and maps does not imply the expression of an opinion on the part of Agora Energiewende concerning the legal status of countries, territories or their authorities. It is without prejudice to the status of or sovereignty over any territory, or to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.